Don’t Let This DRIFT: Why Drift Protocol Will Accelerate as Solana’s All-in-One Exchange

By Rylan Fegan

Disclaimer: This piece was written in October of 2025, before the launch of the Villanova Blockchain Substack this December

Thesis

Pro-digital asset regulation is accelerating the migration of global traders to on-chain venues, fueling demand for seamless, VPN-free platforms that combine low fees with high-yield APY products. Drift Protocol has emerged as the leading perpetuals DEX on Solana, and is now executing on a broader vision to become the All-in-One DEX. Not only will Drift continue to dominate this space, but the protocol positions itself to capture institutional share through Drift Institutional and tokenized equity partnerships, as well as aggressive expansion into real-world assets, prediction markets, and next-gen yield products. As on-chain trading, yield, and regulatory clarity grow, I expect DRIFT to outpace competitors and become the premier hub for retail and institutional capital. I am initiating a BUY position with a price target of $2.66.

Category Overview

In late 2024, a16z reported that only 5-10% of Crypto holders are on-chain, leaving the total addressable market for decentralized derivatives vast; as even modest increases in on-chain adoption could unlock trillions of dollars in new DEX volume. This year, the total derivatives trading volume is expected to reach $60 trillion; and when comparing to centralized exchanges, Decentralized Exchanges (DEXs) is rapidly growing from 1% of global perpetual trading in 2022 to over 2.5% today.

However, decentralized derivatives markets have historically failed to meet institutional traders’ needs for speed, efficiency, and reliability. Legacy Automated Market Maker (AMM) designs have created structural weaknesses and poor capital efficiency that made them impractical for high-frequency or large-scale trading. On-chain exchanges that attempt to solve this also inherit blockchain limitations, such as slow transaction speeds and restricted computational capacity. Attempts to port centralized exchange infrastructure directly onto blockchains have resulted in inefficient designs that discourage market-maker participation.

These headwinds have kept the perpetual DEX market under pressure, with the sector down 35% year-to-date. While there have been notable short-term winners in the space, such as Hyperliquid, the market is looking for a protocol that can operate without the need for VPN access, a long-term winner built on a widely accessible blockchain like Ethereum or Solana, capable of delivering institutional-grade performance.

General Background on the Protocol

Drift Protocol is an open-source decentralized exchange built on Solana, offering low slippage, low fees, and minimal price impact for every trade. Through its decentralized features, all deposits, withdrawals, and trades are executed transparently on-chain, with no off-chain matching engine or any part of the stack off-chain. The execution of all trades is facilitated by smart contract technology with no human or third-party input to execute or fill trades.

Drift Protocol advertises itself as an All-in-One DEX, providing the following services:

Drift Protocol’s MOAT lies in its multi-layered liquidity architecture, integrating a distributed limit order book (DLOB), a just-in-time liquidity (JIT) auction system, and an automated market maker (AMM) backstop. Unlike a central limit order book, which consolidates all orders in a single location, a distributed order book spreads this information across various nodes, further enhancing transparency and reducing manipulation risk. Keepers manage on-chain limit orders off-chain, triggering them when specific market conditions are met to maintain a persistent pool of resting liquidity. The JIT mechanism routes each market order through a short Dutch auction in which market makers compete to fill trades at optimal prices, ensuring efficient execution with minimal slippage. When neither DLOB nor JIT liquidity is available, the AMM maintains constant market depth using a constant product formula, adjusting bid-ask spreads based on inventory levels and allowing user participation in liquidity provision. This triad enables Drift to offer deep, computationally efficient, and decentralised liquidity without relying solely on external market makers.

Drift prides itself on capital efficiency while ensuring protection for your assets. This is achieved through a sophisticated cross-margined risk engine that safeguards against overextension of risk. In the lending and borrowing markets, users have greater flexibility in the supported assets they choose as collateral for both perpetual futures and spot trading, enabling more efficient capital deployment across all products.

Additionally, every token deposited on Drift is eligible to earn additional yield through the protocol’s lending markets while simultaneously serving as collateral for perpetual swaps. Drift currently offers over 10% yield on stablecoin deposits, one of the highest rates across DeFi platforms, so when capital is not actively being deployed in trades, it continues to generate returns. Borrowers are only allowed to borrow if they have more collateral than needed, and a rigorous set of safety measures, such as mandatory overcollateralization and insurance module, ensuring protection for all participants. This approach makes Drift uniquely positioned to offer comprehensive asset protection in a single, seamless trading environment.

What DRIFT Protocol Offers

Drift Protocol leverages Solana’s 100 millisecond finality to deliver industry-leading speed and reliability, and with a 99% in failed transactions this year users can react instantly to market moves and trades with exceptional precision. Traders have the flexibility to choose their own risk exposure, with leverage options configurable up to 101x, and Just-in-Time (JIT) liquidity that ensures that orders of any size are matched at near-zero slippage even during periods of intense volume or volatility.

This trading experience will benefits from October’s Drift V3 upgrade, which according to cofounder Cindy Leowtt introduces “10x improvements in speed, liquidity, and UX; new liquidity source (Drift Liquidity Provider); improved trade reliability with the new orderbook; and scalability with Solana rollups like Alpenglow and Jito BAM”—all designed to set new standards in decentralized derivatives infrastructure.

In addition, Drift recently launched a zero-fee trading program for Bitcoin and Ethereum perpetual contracts. During this campaign, takers and makers can trade BTC-PERP and ETH-PERP with no fees, offering an unmatched value proposition for traders and attracting substantial volume from competitors who struggle to match the combined efficiency and cost of Drift’s platform. The positive impact of these innovations is evident in Drift’s financial results: Quarterly revenue more than doubled, rising from $3.05 million in Q2 2025 to $6.51 million in Q3 2025, while TVL has hit an all-time high of $1.3 billion.

In the roadmap, Drift is finalizing Custom Market Leverage, which will soon allow users to intuitively set their leverage per market or position, improving trade form and ROI tracking for those familiar with CEX platforms. Also, while Drift supports cross-margin trading, it is developing isolated positions for traders to allocate specific collateral to manage risk more precisely. Isolated positions require significant changes to Drift’s risk engine and are still under review and testing before release. These updates will help to improve user experience, increase users and capital into the Drift Ecosystem, and generate higher fees and revenue for token holders.

Drift’s Institutional Push

Earlier this year, Drift introduced Drift Institutional as the gateway for bringing off-chain assets into DeFi. The protocol partnered with the Apollo Diversified Credit Fund, ACRED, enabling the institutions to tokenize large fund positions on Solana and access advanced yield automation, leverage vaults, and direct stablecoin borrowings. Drift’s isolated pool structure and integration with established partners like Securitize ensure compliance and Gauntlet-managed strategies can help offer sophisticated, risk-adjusted yields far beyond traditional staking. For Drift, continuing these partnerships can provide value for the $DRIFT token through higher protocol TVL, steady flows of institutional capital, and fresh sources of fee revenue that accrue back to holders.

In September 2025, Drift partnered with FORD’s in the listing of its NASDAQ-listed tokenized equity. Additionally, that week Gauntlet partnered with DefiDevCorp, the first publicly traded Solana Digital Asset Treasury, to move their treasury and the dfdvSOL LST beyond traditional staking into advanced, risk-adjusted yield strategies on Drift Protocol. With millions of SOL on its balance sheet, these equities represents billions in Solana ecosystem exposure. Now, that equity can be deployed back into Drift DeFi - borrowed against, levered, and used in on-chain strategies.

This could be the beginning of Drift becoming the gateway for deploying regulated, yield-bearing RWAs on Solana, which commands a 95.6% market share in the tokenized equity segment despite only having a 3.45% market share in the entire on-chain RWA space. Asset issuers gain deep liquidity, full composability with on-chain strategies, and the ability to interact with both retail and institutional. For the Drift protocol, every new equity listing expands the breadth of usable collateral, increases trading volumes, and drives protocol fee generation.

As this flywheel accelerates, Drift is positioned to strengthen its business fundamentals on both the institutional and tokenized asset fronts. With institutional appetite for compliant DeFi solutions growing, Drift stands to benefit through rising TVL, diversified liquidity, and fee expansion. These launches could propel Drift to the next chapter: capturing greater share of the tokenized treasuries, public equities, private credit market on Solana, directly benefiting the underlying DRIFT token ecosystem.

How DRIFT extracts Value

Drift Protocol generates revenue from multiple sources: taker and maker trading fees (0.02–0.035% for takers, 0.05% spot taker, –0.02% spot maker), vault performance and management fees, and borrowing interest rates. Over the past year, Drift recorded $92.68M in annualized fees and captured $47.3M as protocol revenue.

The revenue pool is funded through several distinct flows:

Borrowing fees from the margin/lending markets

Trading and swap fees from spot and perpetual markets

Fees assessed during liquidation events

These revenue streams are directed to several destinations:

The insurance vault, which acts as a backstop to support user balances and trading integrity during market disruptions

The perpetual market AMM, which periodically draws revenue to incentivize liquidity or manage risk exposure within strictly governed limits

The spot market revenue pools, supporting yield for stakers across different token products

Additional portions of protocol fees fund the spot market revenue pool, where individual token pools (e.g., USDC, SOL) distribute revenue based on governance settings, vault products, and user activity. Other key revenue recipients include insurance fund stakers and participants in the perpetual market AMM. Currently, only staked tokens accrue these rewards; non-staked tokens are not entitled to protocol revenue, though this is subject to change.

Spot and perp market parameters are designed for transparency and governance flexibility. In spot markets, revenue allocation factors (total_if_factor, user_if_factor, liquidation_if_factor) determine what share of borrower interest and liquidation proceeds flow to the revenue pool and ultimately to protocol users or remain with the protocol. For perps, the AMM can draw from the revenue pool only up to defined thresholds, and insurance fund drawdowns are also capped to protect overall protocol solvency. If losses exceed available backstops, the protocol may socialize losses across market participants.

Recent and upcoming ideas from Drift Founders, such as DIP-8, seek to rebalance fee distribution, notably reducing the insurance fund’s share and allocating a portion (e.g., 10%) to DLP holders who supply liquidity and absorb risk in Drift’s virtual AMM. Discussions are also active about shifting toward 100% protocol fee buybacks, which could further enhance DRIFT token value accrual. All protocol fees, including trading, lending, and float income, remain subject to redistribution or buybacks as determined by governance.

Tokenomics

Drift Protocol allocated approximately 12% of its total token supply (1 billion DRIFT) through its initial token generation event in May 2024, distributing 120 million tokens to roughly 150,000 eligible wallets. Currently, only 30% of total DRIFT tokens are unlocked, however, 53% of the total supply that needs to be unlocked is reserved for community and ecosystem growth initiatives, signaling future dilution but also long-term commitment to user acquisition and protocol development. Over the next year, approximately 280 million tokens will be unlocked, expanding circulating tokens from roughly 300 million to 580 million. The aggressive supply expansion over the next 12 months is a notable headwind and will require strong trading volume growth to offset dilutive impacts on token price.

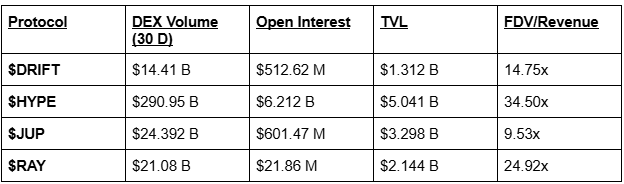

Comparable Protocols

Valuation

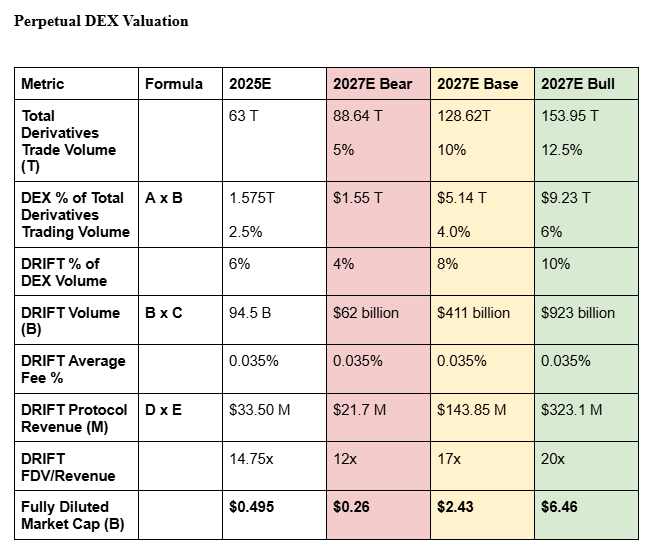

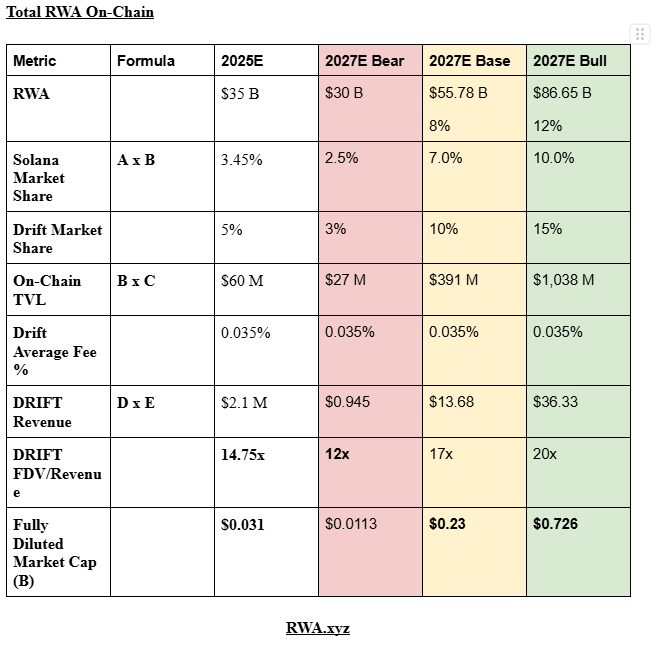

To value a multi-vertical protocol like Drift Protocol, we apply a Sum-of-the-Parts (SOTP) model, breaking down two distinct value drivers:

Perpetual DEX revenue which generates current cash flows through derivatives trading.

Total RWA On-Chain Ecosystem and how much of this will flow into the Solana ecosystem and then specifically the Drift Protocol ecosystem.

As a note, this is assuming that Drift Protocol will propose and finalize a governance proposal to unlock 100% token buybacks for the community.

Based off these valuations, my base price target for Drift Protocol is $2.66, which is a 350% upside from current prices but only 56% higher from its previous ATH set in November of 2024. The bear case price target is $0.27, a 54% downside, and my bull case price target is $7.18, a 1159% increase from the current price.